Why Your Credit Score Matters

Credit scores are a crucial part of financial life, impacting everything from securing loans to renting an apartment. Understanding your credit score and its significance is one of the most important steps in preparing for a mortgage. Let's break down what a credit score is, why it matters, and the key factors that determine this important number.

In the mortgage industry, the specific type of credit score used is called a FICO Score — created by the Fair Isaac Corporation. FICO scores range from 300 to 850, with higher scores indicating stronger creditworthiness.

Credit Score Ranges

Here's a general breakdown of how FICO scores are categorized:

Poor

300–579

Fair

580–669

Good

670–739

Very Good

740–799

Excellent

800–850

Why Is Your Credit Score Important for Mortgages?

Interest Rates

Lenders offer lower interest rates to borrowers with higher scores — potentially saving you thousands over the life of your loan.

Loan Approval

A higher credit score improves your chances of mortgage approval. A low score can make it challenging to qualify.

Down Payment

A strong credit score can reduce your required down payment. Lower scores may require larger down payments to offset lender risk.

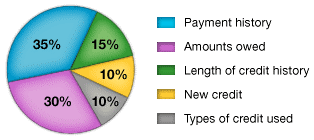

Factors That Determine Your Credit Score

-

35%

Payment History — The most influential factor. Reflects whether you've paid bills on time. Late or missed payments have a significant negative impact.

-

30%

Credit Utilization & Amounts Owed — How much of your available credit you're using. Keeping this ratio below 30% is ideal for a healthy score.

-

15%

Credit History Length — A longer credit history demonstrates experience managing credit. Considers the age of your oldest account and the average age of all accounts.

-

10%

Types of Credit Used — A diverse mix of credit accounts (credit cards, installment loans, mortgages) can positively impact your score by showing responsible management.

-

10%

New Credit Inquiries — Each new credit application creates a hard inquiry. Multiple recent inquiries can signal risk and potentially lower your score.

Additional Factors to Consider

Public Records — Bankruptcies, tax liens, and civil judgments can significantly damage your credit score.

Collections — Accounts sent to collections due to non-payment will have a serious negative effect on your score.

Authorized User Accounts — Being added to someone else's credit card can help or hurt your score depending on their payment history.

Student Loans in Forbearance or Deferment — While not impacting payment history directly, lenders may consider deferred loan status when assessing creditworthiness.

In Conclusion

Your credit score is a critical component of your financial life. It affects your ability to obtain loans, the interest rates you're offered, and even your rental and employment prospects. Understanding what determines your score is the first step toward managing and improving it.

At Contemporary Mortgage Services, Inc., we're here to help you navigate the world of credit scores and financial well-being. Whether you're looking to boost your credit or maintain a strong score, we have the resources and expertise to guide you.

Additional Credit Resources